Transitioning a property into a holiday rental is a long-term investment that comes with a specific and significant set of expenses. As highlighted in our recent meeting, a successful operation requires a clear understanding of the costs that impact the owner's net income.

Here is a breakdown of the expenses you must factor in when planning a short-term rental setup:

1. Initial Setup and Furnishing Costs

The first and most critical investment is in the property's presentation.

Significant Investment in Quality Furnishings: Setting up a property is "quite expensive." You cannot use "granny's leftover furniture." You must make a significant investment in high-quality furnishings to ensure the property looks "excellent compared to everything else." This is necessary to attract high-end holidaymakers and business travelers and, crucially, to avoid "undesirable bookings" from undesirable clientele (like people seeking a party venue or hourly stays).

Extra Inventory in Storage: In addition to quality furnishings, you will also need to maintain extra inventory in storage to replenish items that might break, such as extra cutlery, crockery, and bedding. This constitutes an additional, necessary cost.

Property Preparation: The extensive initial setup also involves creating an outstanding guest experience, which includes professional photos, detailed descriptions, and developing an onboarding document or guide with local area tips, emergency contacts, and clear directions—all essential for securing a high star rating (4.8+ or five-star).

Security & Access: An advanced key system is highly recommended, such as installing an electronic lock that connects to Bluetooth and enables access via a shared code, to prevent the risk of lost keys.

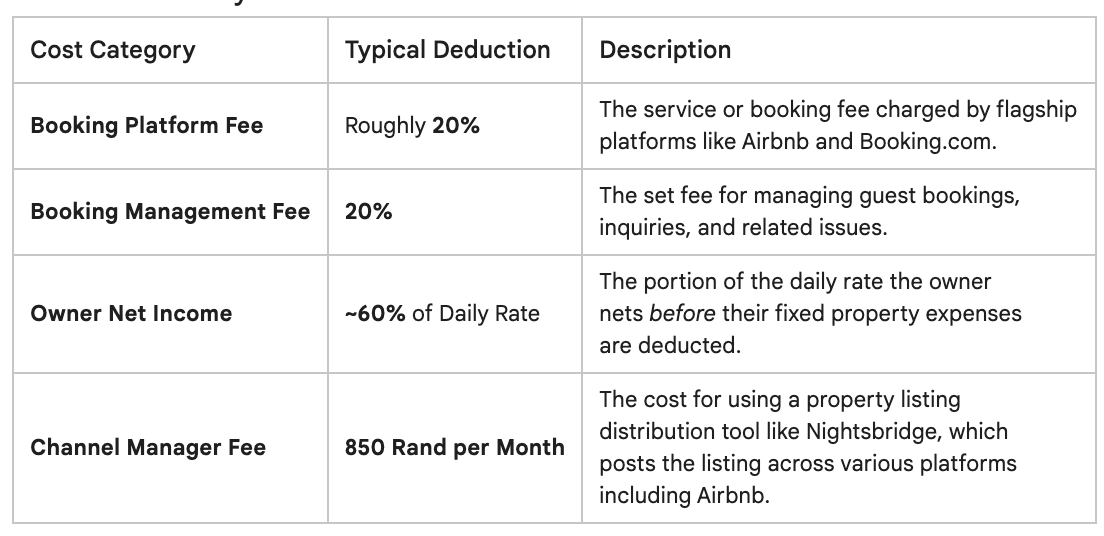

2. Ongoing Fees and Deductions

The gross advertised price is subject to several layers of fees that drastically reduce the owner's monthly take-home income.