The sector is growing. The problems are growing faster. Here's how to invest intelligently.

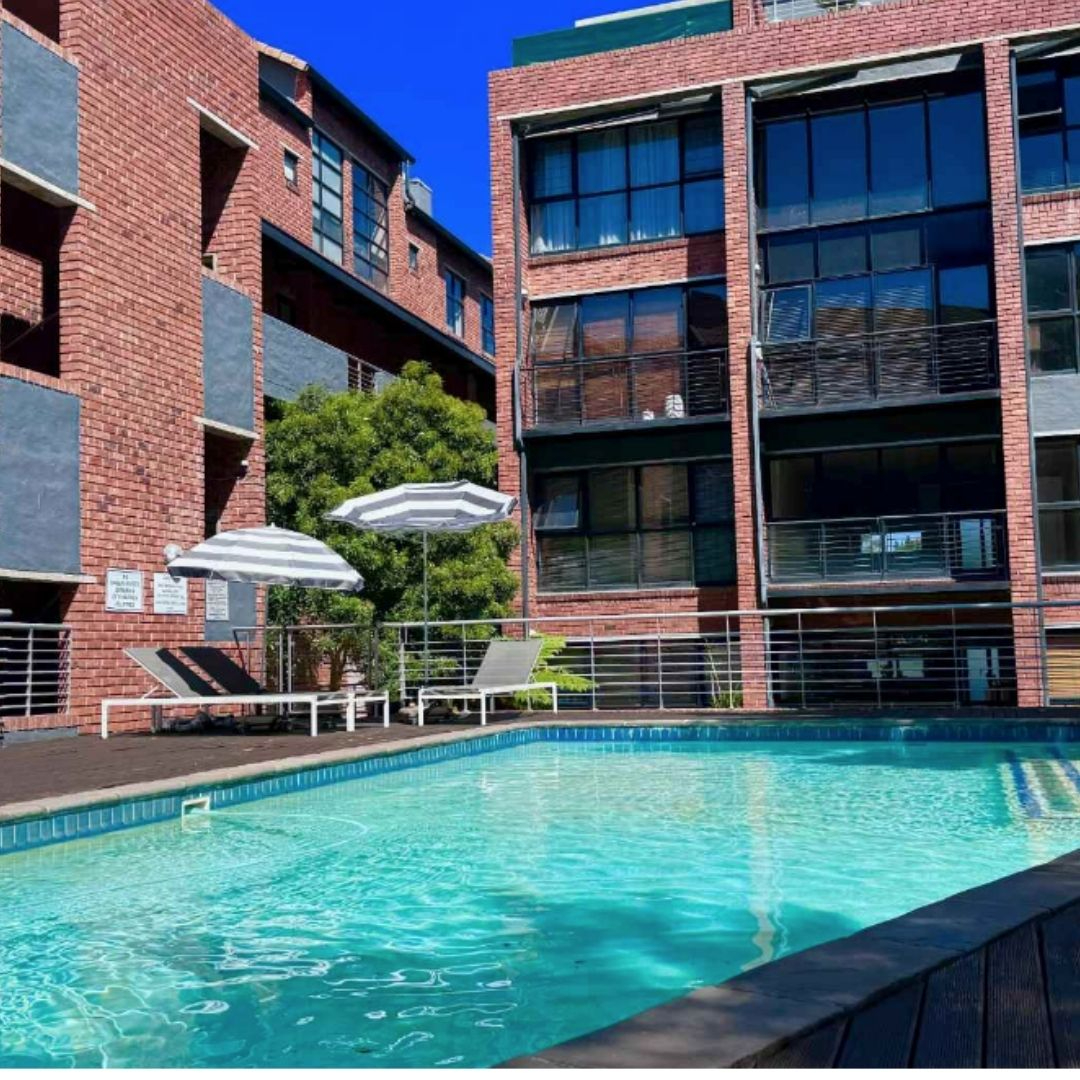

Sectional title is one of the most accessible entry points into South African property investment. Lower purchase prices relative to freehold. Built-in security. Shared maintenance costs. Rental demand driven by the same factors — affordability, security, convenience — that make these properties attractive to buyers.

The number of sectional title schemes in South Africa has reportedly doubled over the last decade, from around 60,000 to approximately 120,000. The sector is not shrinking. It is not declining. It is one of the fastest-growing segments of the property market.

But growth in volume has not been matched by growth in governance. And for investors who don't understand the risks embedded in the sectional title environment, the gap between the apparent opportunity and the actual return can be significant.

Here is an honest assessment of both sides.

The Investment Case for Sectional Title

Accessibility. In most markets, a sectional title unit requires a smaller capital outlay than a freestanding property. For investors building a portfolio, this allows for broader diversification across multiple properties and areas rather than concentration in a single asset.

Rental demand. Security, affordability, and communal amenities make sectional title complexes consistently attractive to tenants. In urban centres and near business nodes, demand for well-located sectional title rentals remains strong. Vacancy risk, where the property and scheme are well managed, tends to be lower than for comparable freehold properties.

Shared maintenance costs. The body corporate absorbs the cost of maintaining common property — the roof, the gardens, the security, the external structure. For an investor, this removes a significant category of unexpected expense that freehold ownership carries.

Security. The gated, access-controlled environment that characterises most sectional title schemes is not just a lifestyle feature. It is a tenant retention feature. Tenants who feel safe stay longer.

Growing market. With 120,000 schemes and growing, the market for sectional title — both as a place to live and as an investment product — shows no sign of reversing. Urbanisation, affordability pressures, and security concerns continue to drive demand toward the scheme living model.

The Risks That the Brochure Doesn't Mention

The levy non-payment crisis. When Stratafin began analysing schemes in 2014, levy non-payment across South Africa sat at around 5%. Today that figure is between 25 and 30%. One in three sectional title owners is not contributing to the maintenance and running of the scheme.

For an investor, this matters in two ways. First, it affects the scheme you're already in — if a quarter of your neighbours aren't paying, your levies will rise to compensate and your scheme's maintenance will suffer. Second, it affects every scheme you're considering buying into. A scheme with a large arrears book is a scheme whose future costs are going to land on the owners who are paying — which, after you buy, includes you.

You inherit the scheme's obligations. When you purchase a sectional title unit, you become a member of the body corporate. You inherit its financial position. A scheme that owes R2 million to the city, that is facing a major roof replacement with no reserve fund, or that has 30% of its levy book in default — all of that is now partially your problem.

This is not hypothetical. Special levies are raised. Municipal accounts fall into arrears. Maintenance is deferred and then catches up in expensive bursts. The investor who didn't check the financials before purchasing discovers these realities in their first year of ownership.

The small scheme premium. The fewer units in a scheme, the higher the levy per unit tends to be — because fixed costs are divided among fewer payers. A scheme with 10 units and a night security guard pays a higher per-unit cost for that guard than a scheme with 200 units. This affects the net yield on the investment and, at high enough levels, affects the attractiveness of the property to prospective tenants.

Governance risk. Schemes are run by trustees — owners who volunteer their time and who may or may not have the knowledge, commitment, or availability the role requires. A poorly governed scheme makes bad financial decisions, defers maintenance, fails to collect levies, and allows the physical and financial condition of the development to deteriorate. The investor whose return depends on a well-maintained, well-managed complex has a genuine exposure to trustee quality.

Liquidity constraints. A sectional title unit in a scheme with known financial problems, unresolved governance issues, or a deteriorating physical condition is a harder sell than a comparable unit in a healthy scheme. Investors who need to exit may find their options constrained — particularly if the scheme's financial position means bond applicants can't get approval.

What Stratafin's Model Reveals About the Market

Stratafin's core business — purchasing outstanding levy debt from schemes and pursuing recovery through the courts — offers a useful lens on the health of the sector.

When the company started in 2014, the debt purchase opportunity was relatively modest. Today, Willie Roos describes demand that has grown to the point where Stratafin has become selective, focusing on the mid-to-upper market where unit values exceed R1.5 million and individual debts exceed R50,000. They have over R200 million in smaller debt purchase requests that they have chosen not to pursue because the business has more opportunity than it can absorb.

This is not a picture of a healthy sector. It is a picture of a sector under significant financial stress, where the gap between what schemes are owed and what they can collect has grown large enough to support a substantial specialised recovery industry.

For investors, the implication is clear: the quality of the scheme matters enormously. A scheme that collects its levies, maintains its reserves, keeps its financials current, and has engaged, competent trustees is a fundamentally different investment from one that doesn't. The purchase price of the unit may be identical. The investment outcome will not be.

How to Invest Intelligently in Sectional Title

Do the due diligence on the scheme, not just the unit. Request the audited financial statements, the debtors report, the 10-year maintenance plan, and the maintenance reserve fund balance. Read them. A scheme with a clean levy book, a funded reserve, and current financials is worth more — as an investment — than a comparable scheme that is struggling, even if the unit prices appear the same.

Assess the levy trajectory. Is the levy increasing year on year above inflation? If so, why? Levies rise either because costs are rising or because fewer owners are paying, requiring the same expenses to be covered by fewer contributors. The former is manageable. The latter is a warning sign.

Check the scheme's municipal account status. A scheme in arrears with the municipality is a scheme that risks having its services disconnected. This makes the property difficult to rent and almost impossible to sell until the arrears are resolved.

Understand the body corporate's legal posture. Is the body corporate actively pursuing levy arrears through the courts? A scheme with significant arrears and no collection activity is a scheme that is allowing its financial position to deteriorate. Conversely, a scheme that pursues arrears promptly — even if it means some uncomfortable conversations — is a scheme that is protecting its financial health and the value of every unit in it.

Factor levy costs into your yield calculation. The net yield on a sectional title investment is not the gross rental less the bond payment. It is the gross rental less the bond, the levy, the rates, and a realistic provision for special levies and maintenance costs. Run the numbers honestly before you commit.

Consider the scheme size. Larger schemes, all else being equal, tend to have lower per-unit costs and more financial resilience. A scheme with 200 units can absorb 10% non-payment more easily than a scheme with 20 units absorbing the same percentage.

Sectional title remains a legitimate and accessible investment vehicle. The market is growing. Rental demand is real. The shared cost structure has genuine advantages.

But the sector is carrying financial stress that is not visible from the outside of a well-presented complex. The investor who does the work — who reads the financials, checks the arrears, understands the levy trajectory, and assesses the governance quality of the scheme — is the investor who captures the opportunity without inheriting the problems.

The sector rewards informed buyers and punishes complacent ones. Know what you're buying. Not just the unit — the scheme.